San Francisco-based portable installments organization Square has secured a rotating credit office in the low several millions headed by Goldman Sachs with interest from Morgan Stanley, Jpmorgan Chase, Barclays, and Silicon Valley Bank. Square streamlines business transactions for people and organizations with its charge card onlooker, purpose of-offer framework, and individual wallet.

Established in 2009, Square has brought $341 million up in wander financing and will utilize the new obligation financing to reserve development as it anticipates that deals will approach $1 billion not long from now.

Venture capitalist Marc Andreessen, Palantir co-founder Joe Lonsdale and Goldman Sachs COO Gary Cohn sat down today at the Goldman Sachs conference in San Francisco, to talk about the thing investors always talk about: Tech.

The Netscape founder, taking the same stance he’s had for years, was ever the ebullient optimist. (Because what else are VCs paid to do?)

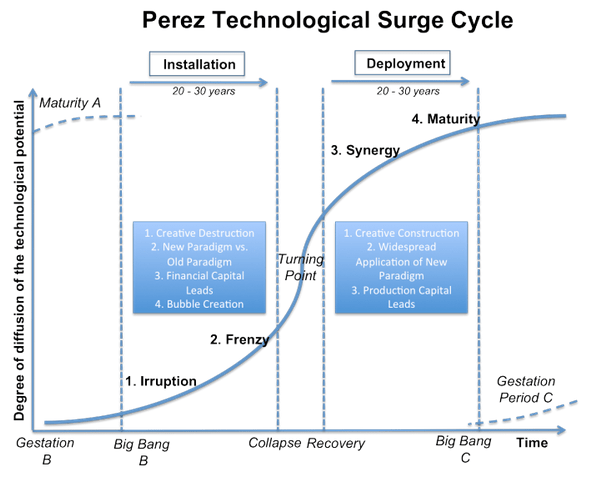

He argued that advances in mobile and chip-making technology signaled exponential expansion of the market. He said tech isn’t overhyped and could have “decades” of growth ahead of it. Echoing economist Carlota Perez’s research, he said world-changing technologies like the web usually settle into a more mature deployment phase after an initial period of hype and investor frenzy.

Andreessen was hopeful about how the Internet of Things could transform the way people live, and credited Moore’s law with the potential to put a chip in everything: “What if we chipped every kid? What if we chipped every dog?”

Both Andreessen and Lonsdale said this Cambrian explosion of software and hardware companies like Anki and Oculus VR (both A16z investments) is a boon for big data and security startups.

Andreessen was basically repeating his famous argument that “software is eating the world.” So Cohn took a moment to remind him that the financial-services industry was the only thing that Andreessen said software couldn’t eat.

Cohn asked if Andreessen has reevaluated his stance, because the investor’s new pet technology is Bitcoin. Cohn said the crypto-currency was like “a pure attempt for software to eat the financial-services industry.”

“I would not encourage your grandmother to put her life savings in it,” he said. “[But] every single smart computer science person I’ve had look into it has reached the same conclusion — it’s a fundamental breakthrough in technology.”

He gushed: “For the first 20 years of the Internet, you couldn’t do this … Bitcoin is the first Internet-native approach of dealing with money. He said that corrupt governments and flimsy central banking systems would be Bitcoin’s true test.

“The prospect of a new technology is a big deal once you get out of the West,” he said.

Lonsdale used Bitcoin as an example of “how industries work” and “how they should work” and views healthcare and education as some of the biggest targets for reform.

“It’s very clear that all these systems were built back in the 70s and 80s. You’re seeing these giant gaps that are being filled in.” He was also weary of social media investments in 2014, because he wants entrepreneurs to make bigger bets.

“Is this something that’s pushing the world towards the way it should be?” he asked.

Andreessen said our current moment in time fits right into Perez’s model of technological and societal change. (She wrote a pretty influential book in the investor community called “Technological Revolutions and Financial Capital.”)

Andreessen said we’re in the “deployment” phase. He brought up Perez’s cycle of new fundamental technologies: At first they’re not taken seriously, then way too seriously, then there’s a financial crash and then the same amount of seriousness.

“Tech is recovering from the depression,” Andreessen said, referring to the 2008 financial crash, and insinuating that we are now in a sweet spot. “The ratio of public tech PEs [price-to-earnings ratios] versus public industrial PEs, tech is undervalued. Relatively, tech PE ratios are really low. I know a tech company with a PE of six. We’re so far away from bubble territory that it’s unfair to compare this to the late 90s.”

Andreessen touched briefly upon recent strife between the tech industry and longtime San Francisco residents. He called recent protests “misguided,” but he seemed sympathetic.

“They are attacking the demand for housing [whereas the discussion should be] around the supply of housing,” Andreessen said. “Market forces want the Valley to expand; if our politicians show leadership, we have decades of growth ahead of us.”

When asked by Cohn the loaded question: “When does a venture fund know when it’s gotten too big?” Andreessen again referred to the broad potential of venture investing.

“For top tiers, the investable universe is only 100-200 companies,” he said, emphasizing that only about 15 of those are hits. “Perhaps that’s the rate in which the economy can support new ideas. Right now we’ve got 15 good ones, but that number could double and VC would need to increase to support it. I can’t wait to see what the answer is,” he said.

“Yeah, I just stare at my desk; but it looks like I’m working. I do that for probably another hour after lunch, too. I’d say in a given week I probably only do about fifteen minutes of real, actual, work.” — Peter Gibbons, Office Space

For whatever reason, explaining this to my high school friends gets two reactions: confusion or their head exploding.

I’ll say it here in plain English — a creator, whether an artist, musician, photographer, craftsperson, marketer, performer, animator, designer, CEO, videographer, or author, can make a living. And anyone — really anyone — has the chance to work on projects they care about and projects that matter to them. They’re not the foolhardy risk-takers you’re taking them to be.

You don’t need to major in accounting, medicine, or engineering to secure a future — chances are, even your safe options won’t do you justice.

It’s a new world out there, and if you’re anything like I was when I was 16, you’re missing out.

How To Be A Slave

“Never let the guy with the broom decide how many elephants can be in the parade.” — Merlin Mann

If you’re not working on projects you care about, you’re risking something that’s greater than yourself. You risk working with people you don’t respect. You risk working for a company whose values are inconsistent with your own. You risk compromising what’s important for a paycheck. You risk doing something that fails to express — or even contradicts —who you are. And then, there’s the shittiest risk of all — the risk of not doing what you want to do, on the bet that you can buy yourself the freedom to do it later.

I know, I know. Dramatic.

But it’s important to think about these things because it’s easy not too — especially as a college student.

It’s easy and convenient to think that a degree is all you need. Good grades, a solid ACT score, a good major, and then, high-paying jobs will fall straight into your ass.

But life is messy.

When everyone is making the same bet, there’s more competition. And when there’s more competition, there’s fewer winners. Those winners range from soul-sucking middle-management at T-Mobile to soul sucking stockbroker at Goldman Sachs.

The money’s different, but the sad man in the uniform is the same.

When you’re fresh out of college, thousands of dollars in debt, and you’re begging (on your knees) for a job on CareerBuilder.com, you’re also competing against 30 year olds who are willing to put their dick on the line (and take a cut in pay) to keep the house and kids.

You’re not going to win by playing by the old rules.

Here’s Why The Adults In Your Life Are Wrong, and Why Times Have Changed

“We are the stories we tell ourselves” — Joan Didion

In the 70’s (when your parents/dinosaurs were around), people who wanted to work on what they care about, barely could. If someone wanted to be a creator or an artist or a writer, they had to be picked by an executive, by an adman, by an audition, and that rarely happened.

Now, we get to pick ourselves.

The pre-90’s were filled with gatekeepers stopping you from doing cool things — you didn’t have access to the studio, the music equipment, the sound-editing board, and the publishing platform unless you were “in” and a fat man in an Armani suit okayed you. Now, even your Macbook comes pre-packaged with free Movie software they didn’t have 10 years ago.

At any moment, anyone can access more knowledge, more tips, more advice, more art, more guidance than the entire Library of Alexandria ever had. Don’t know how to write well? It’s there. Don’t know how to convince a Venture Capitalist? It’s there. Don’t know how to properly put on a condom? It’s there, and I’m not linking that for you.

The tools used to be in the hands of only the top music, film, fashion and business executives. Now, with software, the tools are essentially free. And with the internet, you get a distribution platform.

It’s not just for cat videos anymore. With the internet, came opportunity.

Yet most people don’t make it past Facebook.

You literally just got a license from God to do whatever you want — so use it!

Rethinking What College Means Now

“I went to college for four years” — Kim Kardashian

One of my friends, Edward Druce dropped out of high school. If you were like the 16 year old me, you would havecalled him the fuck out.

But, plot twist, he is absolutely killing it.

I’ve worked for UnCollege. I’ve done industry research on how college defines us — from mental misconceptions to career opportunities.

And yet what I’ve found is that where you go to college does matter —if that’s all you’ve ever done. For the first job, G.P.A.’s will be called into question and kids with Ivy League degrees will be called first, because the degrees they have are shiny and pretty and filled with rainbows and butterflies.

And ultimately, we’re lying to ourselves when we see a kid who got into Stanford, nailed straight A’s, and dismiss them — because that, by itself, says something.

Being not the greatest student, I know how hard that is.

But, looking at the authors I’ve worked with and the people that are happy with what they do, where they went to college matters next to none.

And instead of investing in their degree, they invested more in themselves. They started nonprofits, they worked for Fortune 500 companies, they started businesses, they made art, they marketed, they staged shows, they made music, they made movies, they held Youtube channels, they wrote, they published, but more importantly, they did. And that speaks louder than any G.P.A. or degree could in a heartbeat.

In fact, for many, it spoke so loudly that if their ass had no degree, it didn’t even matter. They were in. (Enter all the college dropouts you hear about in the news, plus the ones you don’t)

When the game is degree vs. degree, it’s easy to lose. But when it’s degree vs “dude who started his own art show”, the equation tips.

“The reality is that in the real world, the things you learn in school vaguely apply and in the real world, past your first job, no one cares about what GPA you have or where you graduated. People want experience. They want to know that they can give you a job and that you can accomplish it. They want to know whether or not you can do what they’ve assigned. In the “real world” you don’t get directions for a lot of things anymore; they give you that job because you need to figure it out. You need to go and figure out that problem and there isn’t a 10-step process for you to follow anymore. If all they wanted was someone to follow rules, then they’d hire a robot.” — Jonathan Chen

Google’s own research have shown that GPA and test scores are ‘worthless’ for hiring. And employers — well, they know this. They know the guy with the art show probably has his shit together.

Ultimately, that’s where the green light is. When they see real world, tangible results, and it says “hey, that guy has his shit together”, they’ll give you the go.

For your parents, college was the only investment that mattered. Now, college or no college, invest in yourself.

[Side note: If you have the money or want to pursue a licensed profession — go to college. It’s a time where you get to be a kid without the responsibilities of being an adult, and that’s fun. Yeah, the job and debt ramifications aren’t ideal — but it’s still a blast and it’s still a time for personal growth if you let it be.]

Suck City, Free Work, and Apprenticeships (or How To Invest In Yourself)

“Always be yourself…unless you suck” — Josh Whedon

The geniuses. The little Mozarts. The born-again Darwins. It’s easy to think that genius isn’t for us and for…well, other people with large foreheads and Walter White glasses.

But the brave new world for creatives changes that. It doesn’t take genius, luck, or an act of God — though a little can’t hurt.

Now, it’s up to us to play the hand.

With the Long Tail and Kevin Kelly’s 1,000 True Fans Model, there’s a niche (roughly 1,000 people) out there waiting to be filled. Before, you either catered to millions or to no one. Now, as Kelly would say, all it takes to make a living is to find your 1,000+ true fans…or work with someone who has.

And this…changes everything (cue dramatic music).

But here’s the truth.

A lot of creators out there suck. They don’t know what they’re doing. We’re all in this boat, and we’re all shaking at the paddle.

My friend, Andrew Edstrom, put the solution nicely [emphasis mine]:

“1000 true fans is flawed because at first most [musicians] produce music that absolutely no one on the planet wants to hear. You don’t know what people want to hear, all you know is what you want to play, so you make a bunch of music that you want to play but no one else wants to listen to. You may love writing 8 minute power ballads that change key, genre, and tempo every other measure, but good luck finding 1000 fans with that. What I’m saying is, beginners produce art for niches that don’t exist.

So no matter what niche of music you plan to occupy, you need to master these basic elements before anyone in the world is going to listen to you. That’s where music lessons (apprenticeship) comes into play. Instead of learning what crowds consistently don’t like through years of playing to 1 or 2 people in an otherwise empty bar and then surveying their reactions, you can learn from someone who already knows what works and doesn’t.

After you’ve mastered the basics, you will understand what the difference really is between different niches. After you put the time in doing your apprenticeship, it will be obvious to you what niche of music needs to be filled by someone. That’s when you winning over 1000 fans begins.”

There’s a way to find the intersection of what you love and what people will pay for. And that’s apprenticeship — working under someone who’s already done what you want to do.

Finding this intersection — and doing it through an apprenticeship — is the most important advice I’ve ever received. I’ve learned more in one month of working under someone that four years of high school. And whether you find an internship where they don’t treat you like the house bitch or you go my route and tap into Free Work (pitching high-profile people to work under them, free of charge), what matters is that you’re learning under someone who’s brilliant, and yeah, “has their shit together”.

It’s not about the money — it’s about the craft, the art.

But bottom line, it’s about what you love to do.

I’m not sure the bank middle-manager really loves his job. Or the 4th grade gym teacher. Because even if he wasn’t being paid, I don’t think he would be typing Excel files or screaming at little people shitting their pants. And seeing how easy it is to slip into a cubicle-coma, that scares me. Not holy-shit-it’s-Freddy-Krueger scary. But still scary.

Closing Thoughts: Bentleys and Dreams

CAROLYN: Lester. You’re going to spill beer on the couch.

LESTER: So what? It’s just a couch.

CAROLYN: This is a four thousand dollar sofa upholstered in Italian silk. This is not “just a couch.”

LESTER: It’s just a couch!

He stands and gestures toward all the things in the room.

LESTER: This isn’t life. This is just stuff. And it’s become more important to you than living. Well, honey, that’s just nuts.

—American Beauty, 1999

Back in ‘07, my plan was to become a doctor.

I was 13. And brown.

But I’d nearly forgotten that old dream. Not because there’s anything wrong with pursuing medicine. It’s actually pretty damn brave. But because there is something wrong with loving the idea of something, rather than actually wanting to do it.

When I thought doctor, I thought about the Bentley that came with it. The saving lives part…?

I’ll take one Bentley please.

Somewhere along the line, we hear relatives, teachers, and guidance counselors tell us about what’s important, about who to trust, about what matters, and think — we know what we want. We’re invincible, after all…

But life is messy.

What matters now is that in this brave new world, we’ve been given the chance to reinvent ourselves. We’ve been given the tools and the access. And once you go past the daring cat videos and Sharkeisha Vines, you’ll start to realize it’s exciting, it’s unreal, and it’s insane.

All we need to do, is move.

“…most men and women will grow up to love their servitude and will never dream of revolution.”

― Aldous Huxley, Brave New World

Be honest. Are you a good engineering candidate? How are you measuring yourself? How many companies have you interviewed at? What is your onsite-interview to offer ratio? Try the following formula (that I’ve totally made up in a vacuum and ultimately means nothing):

# x = number of companies interviewed with onsite

# y = number of offers received

value = 100 * log(x) * y / x

If your value is < 90, you should read this. If it’s > 120, then you probably don’t need this, but should read it anyway.

Who am I?

I don’t have a college degree. I started programming professionally at the age of 19 after leaving Chicago for Southern California. Everything I owned fit in my car; I had $400 in my pocket and a job offer as a junior programmer for a cool $40,000 a year. That was 12 years ago. But that’s another story.

I’ve interviewed at least 500 engineering candidates. Roughly 10% were given offers. Less than 3% I considered “rockstar” candidates, and I remember all of them.

I will tell you that there is absolutely no sure-fire way to getting hired. There are too many variables, especially at a company like Google where you are placed with 5-7 random software engineers and it’s up to them to come up with an appropriate set of questions to ask, usually involving whiteboard coding. Some engineers are terrible interviewers, they ask unfair questions and create snap judgments. But that’s OK, it happens to the best of us. You’re generally allowed to flub a single interview in a panel.

The best I can do is tell you how you can be adequately prepared. So without further ado, here are the tips I can give you.

Technical Tips

Image by None via CrunchBase

ABC (Always Be Coding). The more you code, the better you’ll get — it’s that simple. By coding, you’re practicing. But the best practice is focused practice. Have goals in mind, explore new areas, and challenge yourself. Over time, you should develop a portfolio of both unfinished and finished projects. GitHub is a great place to put this portfolio on display, but just having an eclectic body of work is huge.

Master at least one multi-paradigm language. Mastering a language gives you a great sense of perspective. To do this, you must write a lot of code, read a lot more, and learn the gotchas and best practices. Ideally the language has a vibrant community, runs a lot of production code and is reasonably en vogue. Some good candidates are C#, C++, Java, PHP, Python, and Ruby.

There’s a famous leading question that C++ interviewers like to ask other C++ programming candidates, “On a scale of 1-10, 10 being the highest, how would you rank your knowledge of C++?” I hate this question. And god help anyone who answers a 9-10, because the claws will come out. Bjarne Stroustrap himself would rate himself probably an 8 or less. The language is simply too complex, too rich, and has evolved too much over time. I digress.

Know thy complexities.Read this cheat sheet. Then make certain you understand how they work. Then implement common computational algorithms such as Dijkstra’s, Floyd-Warshall, Traveling Salesman, A*, bloom filter, breadth-first iterative search, binary search, k-way merge, bubble/selection/insertion sort, in-place quick sort, bucket/radix sort, closest pair and so on. Again, ABC. This article is also a good, thorough primer.

Re-invent the wheel. You should implement the most common data structures in your language of choice. Do not rely on common libraries. Implement the following and write tests for them: vector (dynamic array), linked list, stack, queue, circular queue, hash map, set, priority queue, binary search tree, etc. You should be able to implement them quickly.

Solve word problems. Forget queries like this. It all comes down to fundamental programming concepts. Spend at least 40 hours coding solutions to different types of problems. One of the best resources is TopCoder. Read this. Then try solving problems. Pick those that test your ability to implement recursive, pattern-matching, greedy, dynamic programming, and graph problems. Just go through a bunch of archived problems.

This is probably the number one reason I was hired at Google. I spent literally two weeks obsessed with TopCoder. After that, I could code Dijkstra’s algorithm with my eyes closed and one arm tied behind my back. I could solve almost any kind of graph-problem under the sun. It was all problem-solving repetition. And as Eric Schmidt says, “Repetition doesn’t spoil the prayer.”

Make coding easy. At least, make it look easy. Over time, I’ve learned that programming is the most straightforward and simple part of being an engineer. I often use the phrase “a simple matter of programming” because I believe the harder parts of being an engineer is before and after most of the coding takes place. For example, designing what you’re about to code and ensuring what you’ve already coded is shippable and production ready. Make your interviewer understand that you know that programming is just a means to an end.

Note, coding in front of others can be daunting. Find a way to practice both white-boarding and pair-programming. Google is basically all about coding at a whiteboard, whereas Square is effectively all pair-programming at a real machine with your language and IDE of choice. Read this article from my friend and former colleague Dan.

General Tips

I can’t claim to be an expert here. In fact, some would say that I’m not even very good with people. But I should probably speak to some non-technical tips, many of which are probably quite obvious.

Know why you’re there. If you’re interviewing at a company and you don’t fully understand why they exist, who they are, or what they do; then don’t do it. Engineers who care about the hires they make will smell it a mile away. You may be able to get away with this at bigger corporations, but it won’t fly at smaller ones.

Be passionate. If you don’t care, then nobody else will. Be passionate about something. It might be programming, but what about it? Do you enjoy building compilers in your spare time? Do you build and fly RC helicopters? It doesn’t really matter because if you’re passionate about it, then you can make it interesting.

Don’t make assumptions. Ask questions if you’re not sure. If you’re asked a question and you aren’t 100% certain what the problem is, then ask. There are a number of times where I’ve seen a candidate go down some path, never ask a question and ultimately waste time solving the wrong problem.

Smile. Be excited, happy and positive. But don’t overdo it. As I mentioned before, people will make snap judgments. Make sure your first impression is a good one. Smiles are infectious, I’ve often walked into an interview in a bad mood or feeling overwhelmed with other priorities, but a well-placed smile from a candidate quickly snapped me out of it.

As I said before, there’s no silver bullet to getting hired. But, as an engineer, the best thing you can do is to ABC: Always Be Coding.

Love or hate this article? Let me know @davidbyttow.

*Today, I work for myself. Building something new.

Starved for scoops, many don’t bother to check the veracity of revenue and profitability numbers for non-public and pre-IPO entities before printing them

I’m noticing more numbers no one checked reported as “breaking news” or adding spice to puff pieces with potentially hidden insider agendas. Maybe some journalists are intoxicated by access to the non-public numbers some would pay a lot to know for sure. Maybe it’s just too hard. Worst case scenario journalists can be used as cogs in the equity market pump and dump machine.

Summary level revenue and profitability numbers for public companies, those listed on U.S. stock exchanges, are easily verified. Go to the SEC filings —10-K annual reports, 10-Q quarterly filings, 14A annual proxies, 8-K filings of other legally required to be reported events — to see if what an executive says matches what he or she told regulators and markets in the filed financial statements. Even earnings calls and earnings releases should match what’s eventually filed or executives must later must explain why not.

Readers may think that online or in print, whether in a magazine or a newspaper, writers have to check the truthfulness of what politicians and business executives say before they print it. More and more they don’t. Intensely partisan rhetoric during the last election cycle led to complaints on both sides that major media allowed politicians and their operatives to make claims about each other in debates, in print and online that weren’t true. Lies took on a life of their own. “Unspilling the milk” was almost impossible. A cottage industry of political fact-checkers —FactCheck.org, Politifact, and media-watching bloggers and journalists — scoured public statements and news and magazine articles for blatant, and not-so-blatant, examples of lies and fibs that slipped into campaign season reports.

There’s no such service dedicated to checking non-public and pre-IPO financial puffery and blustering. The hype before the Facebook IPO is an example of unverified financial information gone wild. When the New York Times broke the story of Goldman Sachs’ investment in Facebook on January 2, 2011 it was obvious a certain segment of the investing population willingly ignored the lack of audited, verifiable, complete financial information when offered a “hot and exclusive” opportunity. The media was more than willing to repeat unaudited, unverified, and often incomplete information in its stories, true or not. Reuters eventually reported that disclosures provided to Goldman Sachs’ chickens, I mean clients, intended to entice them to make a $1 million minimum investment, weren’t even audited results.

A casual attitude by business journalists towards verification of not-ready-for-prime-time financial “leaks” has spread to reporting on “new” media business models. Merely repeating positive results seems to be enough to make them so. Maybe that’s why so many accepted “at his word” the recent claims of “profitability” by BuzzFeed founder and CEO Jonah Peretti.

Peter Kafka, the media reporter for Dow Jones & Co’s All ThingsD site, says Peretti’s public-private memo to employees is

full of boast-worthy boasts: A ton of page views, a lot of employees, and a profit, to boot.

Peretti, according to Kafka,leaves out the specifics. But then Kafka makes some unattributed boasts of his own about the numbers.

…from what I hear, those numbers are boast-worthy, too.

The column goes on to cite, quite confidently, opinions from “a person familiar with BuzzFeed’s operations” and then “a different person familiar with BuzzFeed’s operations” to substantiate some specific numbers.

Peretti also claims BuzzFeed had 85 million unique page views in August. That’s non-financial but very important data used to estimate ad revenue. TechCrunch’s Anthony Ha gets credit for checking that assertion with comScore. While comScore’s data has its shortcomings, its methods are transparent and thus it’s one of the only sources that provide apples to apples comparisons across different sites. comScore says BuzzFeed had 31.9 million global unique visitors on desktop in July versus Peretti’s 85 million the following month. That’s quite a stretch from one month to the next, if Peretti is to be believed.

Peretti did not respond to my offer, via Twitter, to review the actual financial statements, audited I hope, to verify his claims of profitability.

So who can you trust to fact-check anymore, especially those tough-to-get private company or non-public segment-level numbers? Even the venerable New Yorker magazine will throw a provocative piece of quantitative data into an article with no attribution. In a recent piece that chiefly focuses on a qualitative assessment of whether or not cable news channel MSNBC has figured out “what liberals really want”, Kelefa Sanneh’s “Twenty-Four_Hour Party People” sticks a fact-like statement about the station’s revenues and profitability near the end of a ten-page piece without saying where it came from.

Still MSNBC earned more than $200 million in profits last year, on revenues of $442.5 million.

Sanneh lays down the very specific revenue and profitability figures after talking a bit about how cheap it is to run the opinion-driven cable news business model. Apparently, it’s almost costless except for the salaries of on-camera hosts. And subscription fees from cable bundling, where MSNBC gets a piece of every viewer’s request for ESPN and HBO, are like free money.

James Ledbetter, OpEd Editor at Reuters, is as skeptical as I am that MSNBC is so profitable, but he’s more apt to believe the New Yorker wouldn’t print the numbers if they weren’t truly so.

Comcast is the publicly traded conglomerate that now owns 100% of NBCUniversal. NBCUniversal assets are now spread amongst more than one reporting segment in Comcast’s latest annual report. One of those reporting segments, cable networks, covers 15 national cable networks, 11 regional sports and news networks, various international channels, a cable television production studio, and related digital media properties. One of the cable networks is MSNBC. There is no break out of revenue and profitability figures for MSNBC in the Comcast public filings.

I called Sanneh to find out where he got the MSNBC revenue and profitability numbers in his story. He told me the estimates, not actual numbers, were previously published along with estimates of Fox News and CNN revenues and profits in the 2013 Pew Research Center State of the Media Report. Pew’s source is a firm called SNL Kagan but where does SNL Kagan get the non-public data?

SNL Kagan’s insider knowledge and perspective is what makes our proprietary data so unique and so essential. We provide detailed operational information and exclusive insight that simply isn’t available from any other source.

Sannah said he checked the SNL Kagan estimates with MSNBC sources who “didn’t try to stop the magazine from publishing them”. In fact, MSNBC sources suggested MSNBC profitability may be higher than the estimates. Sanneh went with the research firm numbers since higher company estimates could not be corroborated.

Sanneh and the New Yorker did not identify the numbers as estimates nor did they say where they came from because, according to Sanneh, they had been widely disseminated in the industry. The focus of the article was MSNBC’s editorial philosophy not its financial success.

New Yorker magazine is widely considered by journalists, and the schools that produce them, as the gold standard in fact-checking. In September of 2012, Columbia Journalism Review Books and Columbia University Press released The Art of Making Magazines: On Being an Editor and Other Views from the Industry. Chapter five, “Fact-Checking at the New Yorker,” is taken from a lecture delivered by New Yorker fact-checking director Peter Canby on February 28, 2002.

To start checking a nonfiction piece, you begin by consulting the writer about how the piece was put together and using the writer’s sources as well as our own departmental sources. We then essentially take the piece apart and put it back together again. You make sure that the names and dates are right, but then if it is a John McPhee piece, you make sure that the USGS report that he read, he read correctly; or if it is a John le Carré piece, when he says his con man father ran for Parliament in 1950, you make sure that it wasn’t 1949 or 1951…

Business journalists are asking readers to trust they’ve done some due diligence before printing non-public financial information. I think those journalists, and their readers, should be more skeptical in the future of what they hear and what they read.

AngelList is certainly in the driver’s seat for the biggest change to hit venture in decades. With the release of AngelList Syndicates, and the absolutely perfect timing of the SEC’s changes to Regulation D Rule 506c, AngelList has dramatically lowered the cost of raising capital and has made tech ask a very serious question:

If I’m raising money as an early stage startup, why do I need venture capitalists when I could just go through AngelList?

Image via CrunchBase

AngelList certainly provides a lot of benefits over the traditional VC approach. Unlike venture, AngelList is much more democratic in how you can approach investors. You don’t need to be invited to a Goldman Sachs conference or stalk VCs at SXSW to get an intro to an accedited investor on AngelList. Raising a round on AngelList can also be a lot faster than the traditional due dilligence process at a venture firm, reducing the amount of time that a startup’s executive team needs to spend distracted by their fundraising.

(Reuters) – BlackBerry Ltdco-founderMike Lazaridis has increased his stake in the struggling smartphone maker and is considering buying the entire company, according to a securities filing on Thursday.

Lazaridis, who now controls 8 percent of the company, has engaged Goldman Sachs and Centerview Partners LLC to assist with a strategic review of his stake. He held almost 5.7 percent as of the end of 2012, according to Thomson Reuters data.

The filing said that Lazaridis, who stepped down as co-chief executive and co-chairman of the company in early 2012, made the move along with his fellow co-founder Douglas Fregin.

Six years ago, an unknown Frenchman named Fabrice Tourre was a 28-year-old kid living the dream as a highly paid salesman at Goldman Sachs (GS). Today, “Fabulous Fab” is now internationally known for defrauding investors over a $1 billion in mortgage bond deal that blew up.

Since this was a civil trial, not criminal, Tourre was found liable by a Manhattan jury and will be subject to fines and the possibility of a lifetime ban from the securities industry; a business that is probably not brimming with offers for a convicted expat with a PhD in finance.

As my co-host Jeff Macke and I discuss in the attached video, while this trial took on outsized importance and garnered disproportionate coverage given the relatively small fish in the dock, it is clear that it won’t be the last case the Feds bring forth.

“Guys like him at Goldman should be terrified,” Macke says. “I like this ruling but my problem with it is that it takes away the attention from where it should be, which is much higher up the chain.”

To be clear, Goldman settled with the SEC over the same matter in 2010, paying a record $550 million fine and admitted it made a mistake by selling an investment to one client without disclosing that another client (hedge fund manager John Paulson) had secretly built it to fail.

For the SEC’s part, the case marks a big win and the first time that Wall Street’s top regulator has won a jury trial related to fraud and the financial crisis.

Even so, nabbing Fab is highly unsatisfying and garners little more than a shoulder shrug in many circles. As Macke says, “I’m fine with (Tourre) being prosecuted. It’s a witch hunt. They looked for a scapegoat. But I want the top. If you’re going to send a message, you’ve got to go after the big wigs too.”

Facebook may be more than a place where parents look at pictures of each other’s kids while posting links to various details about their lives and opinions.

Last week’s surprisingly strong earnings report suggests Facebook (ticker: FB) might offer investors a spring-loaded way to monetize the mobile-technology advertising market that so many people believe is the next big thing.

Facebook reported second-quarter total revenue of $1.81 billion, a 53% increase year-over-year, and up 38% from March earnings. “The fact that the beat was driven entirely by advertising revenue makes the outperformance even more compelling, with ad-revenue growth of 61% year-over-year (consensus 40%),” Heather Bellini, who follows the company for Goldman Sachs, advised clients in a recent note. She raised her price target to $46 from $40.

News Corp. (NWS -1.20%) is sure talking a good game, planning to challenge LinkedIn (LNKD -0.68%) and Bloomberg L.P., the parent of Bloomberg News. Many investors, however, are skeptical that the plans from Rupert Murdoch’s (pictured) media empire will amount to much.

Murdoch’s Wall Street Journal is building a challenger to LinkedIn and plans to launch a social network for professionals in coming months, according to the Times of London.

Dating website eHarmony reportedly is considering expanding into job hunting as well, further clouding the picture for News Corp., whose track record in social media includes its disastrous investment in MySpace.

As of the latest quarter, LinkedIn had 218 million members and generated more than 11 billion page views. New members signed up for the service at the astounding rate of more than two per second. Shares of LinkedIn, which have surged more than 45% this year, traded down slightly Wednesday, indicating that Wall Street isn’t too worried about the potential threat from News Corp. Indeed, News Corp. barely budged as well.

And then there’s Bloomberg, a company certainly familiar to Dow Jones CEO Lex Fenwick, who previously worked there as a high-ranking executive. According to Reuters, Fenwick Tuesday spoke to investors about a new product dubbed “DJX” that would compete with Bloomberg and Thomson Reuters (TOC). He also mentioned plans for a messaging system that would compete with Bloomberg’s terminal. Subscribers would get a two-minute jump on news broken by Wall Street Journal and Dow Jones reporters.

Bloomberg News has come under fire after customers such as Goldman Sachs (GS +1.35%) complained that its reporters were snooping on them using data that they had considered to be confidential. Though Bloomberg’s reputation has taken a hit, it’s important to remember that Bloomberg’s competitors have announced so-called “Bloomberg Killers” for years and none have amounted to much.

News Corp. CEO Robert Thompson noted the publishing company has no debt and $2 billion in cash. Of course, News Corp. is taking a write-down of $1.2 billion and $1.4 billion in the current quarter on the value of its publishing assets, some of which, such as The New York Post, reportedly haven’t been profitable for years.

Murdoch has been able to prop up his publishing business with cash cows such as Fox News Channel, which will become part of the new 21st Century Fox. He is downplaying talk that he might buy Tribune’s papers. Indeed, he has a pretty full plate now.

–Jonathan Berr is a former Bloomberg reporter. He doesn’t own shares of the listed stocks. Follow him on Twitter @jdberr.

Mohnish S.

Mohnish S.

David Byttow

David Byttow

Francine McKenna

Francine McKenna

Andy Manoske

Andy Manoske